A summary of the market this month

The overall market for the spot market this month was oscillating, and there was no improvement in transactions. Traders’ operating enthusiasm was not high. From the observation of China Plastic Spot Index, we can see that the spot market this month is still relatively stable, and the range of shocks is not very large. After a certain range of initial highs at the beginning of the month, it basically remains at 1100 points. The main reason affecting the spot trend is the instability of crude oil and crude oil. The three ups and downs of crude oil prices made the business mentality somewhat confused, and they did not dare to judge lightly. Under the support of cost, they refused to ship at low prices. The monomer market basically brought up support to the spot market. Coupled with the fact that petrochemical prices have also remained stable at a high level, by the end of the month, new pricing has been introduced, which has added a lot of confidence to the market. Some regions even have a slight upward trend. However, the downstream buyers are mostly based on on-demand procurement, and the demand is hard to increase. Therefore, there is a phenomenon that the market has no market price.

As of August 31, 2010, the domestic PP, PE total stocks in major markets declined slightly, a decrease of 2.96% from the end of last month and a decrease of 0.74% from the middle of the month. Among them, PP stocks slightly decreased, compared with a decrease of 2.23% at the end of last month and a decrease of 6.78% from the middle of the month; PE stocks declined slightly, a decrease of 0.16% from the end of last month and an increase of 1.18% from the middle of the month. From a regional perspective, southern inventories decreased by 3.7% from the end of last month and a decrease of 0.62% from the middle of the month. Northern inventories declined slightly, with a decrease of 1.45% from the end of last month and a decrease of 0.98% from the middle of the month.

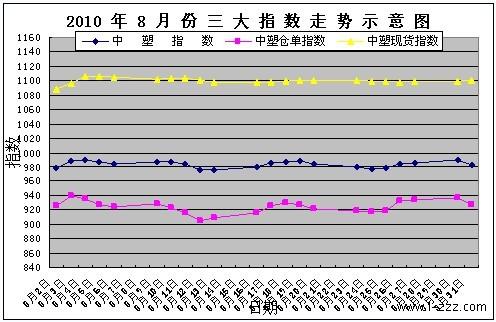

At the end of the month, China Plastics Index closed at 981.99 points, up 10.07 points from the end of last month. China Plastics' spot index closed at 1100.82 points, up 13.6 points from the end of last month. China Plastics warehouse receipts index closed at 924.86 points, up 8.7 points from the end of last month. point.

Second, the review of various varieties of market

1, PE Quote Review

The figure above shows the comparison between the LLDPE/7042/Yangzi petrochemical ex-factory price and the Yuyao Plastics city price trend.

The PE market price in this month had a slight upward trend at the beginning of the month, but it immediately fell into a downward trend. In the middle and later periods, the market trended to be stable. The downtrend of international crude oil did not have a lasting impact on the market, mainly because the low supply of goods and the promotion of the petrochemical industry played an important role in the stability of the market, but the downstream demand had a significant effect on the market, although the market price had declined. However, the overall situation is still at a high level. Buyers wait and see the atmosphere is heavier. The stalemate between the buyers and sellers is obvious, and transactions are general. Businesses are divided about the trend of the market outlook, see more and bearish.2, PP market review

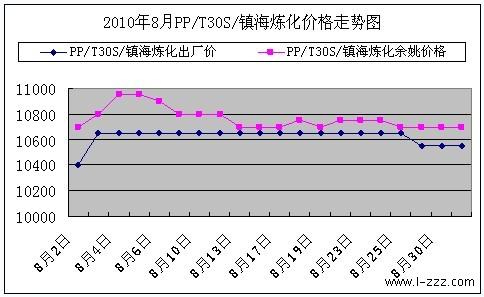

The above chart shows the comparison of the ex-factory prices of Zhenhai Petrochemicals and PP/T30S/Zhuhai in August and the price trend of Yuyao Plastics City.

The PP market price was higher this month than in July. Although the overall market was in a weak consolidation as crude oil continued to decline, there was a short-term spike at the beginning of the month and international crude oil rebounded towards the end of the month, making the market tend to stable. At the beginning of the month, when crude oil rose and the ex-factory price of petrochemicals rose, the market price was pushed up and the atmosphere of speculation was strong. At mid-season, the price of crude oil fell all the way, the market sentiment was hit, the market turned into a downturn, but petrochemicals remained stable, and the business did not want to be low. The market sentiment was thicker in the market; in the later part of the year, the price of oil continued to decline, and the market sentiment was slightly pessimistic. Fortunately, the petrochemical ex-factory price remained strong, and new pricing was introduced at the end of the month, the market was supported, and the price of oil rebounded at the end of the month. The market sentiment has improved. However, throughout the entire month, the market's sluggish demand has hardly improved, and actual transactions have not improved.

3, ABS market review

This month, the ABS market started to rise and stabilized. At the beginning of the month, the company continued its upward growth at the end of July. In the middle of the year, the market began to stabilize. Under the checks and balance of all parties, the market entered a narrow consolidation. In the mid-to late period when the supply of petrochemicals and circulation tightened, the market was high and the market sentiment was relatively stable. Although the correction of crude oil has a detrimental effect on the market, this is not the most important issue this month. Upgrading of petrochemical prices and lack of supply support market prices, and cost support has made it difficult for prices to fall. However, the demand side of the downstream market is still not very optimistic, to a certain extent, inhibiting the market trend.

4, PS Quotes Review

This month, the PS market has changed significantly. At the beginning of the month, following the sharp rise at the end of July, it continued to rise. The upstream cost support was strong, and the petrochemical ex-factory price continued to rise. The supply of the society was tight and the manufacturers shipped more smoothly. However, due to the sharp decline in oil prices, coupled with the lower prices of styrene monomer market, the upstream market has weakened, businesses operating enthusiasm decreased, the atmosphere dropped, and even some businesses cut prices for shipping. Fortunately, in the middle and late, the petrochemical firm factory price is firm, giving the market a certain degree of confidence, less supply, and low-cost sources difficult to find. However, the downstream manufacturers took goods on-demand, poor transactions, the market is in a stalemate, and if the demand side has remained depressed, the real strength of the market is still relatively difficult.

5, PVC market review

The overall performance of the PVC market this month was oscillating up. In the first half of this year, calcium carbide was affected by the knock-out list of post-production capacity of the Industrial and Commercial Group. In the middle period, the supply of calcium carbide was also very tense. The main reason was that the northwest and southwest were affected by the natural disasters of mudslides and the construction started to decline. Because of traffic and transport difficulties, the supply in the mainstream markets of East China and South China was in short supply. Therefore, various factors affect the market to have a significant upward trend, but the trader's mentality is slightly worried, mainly by the downstream demand on demand with the purchase, it is difficult to increase the impact, coupled with the ** and crude oil shocks, traders are difficult to choose At the end of the month, the market price basically stabilized.

III. Review of the trend of international crude oil this month

From the chart above, we can see from the chart of international crude oil prices in July that the international crude oil is in a pullback state this month. At the beginning of the month, the oil price maintained an overall upward trend. However, by the middle of the month, the oil price began to fall sharply and it was close to the 70 mark. Fortunately, by the end of the month, The rise in the stock market affected the rebound in oil prices, and then basically stabilized. WTI quotes fluctuate between 71.63-82.55 USD/barrel this month; Brent quotes fluctuates 72.38-82.68 USD/barrel this month; OPEC quotes fluctuates from 69.69-78.88 USD/barrel this month.

As of the end of this month, the New York Mercantile Exchange's West Texas Light Oil October ** settled at US$74.70 a barrel, down US$3.66 from the end of the previous month; London Intercontinental Exchange Brent crude oil October ** settled at US$76.60 a barrel. At the end of last month, it fell 0.99 dollars.

IV. Upstream monomer review

name

Price type

Quote at the end of July

Quote at the end of August

Change

(US$/ton)

(US$/ton)

(US$/ton)

Asian styrene

FOB Korea

1037-1038

1117-1118

+80

CFR China

1055-1056

1138-1139

+83

Asian ethylene

CFR Northeast Asia

864-866

1010-1012

+146

CFR Southeast Asia

810-812

980-982

+170

Far East Propylene

FOB Korea

1079-1081

1194-1196

+115

May and September Outlook

This month, the international crude oil turbulence was the main declining trend. Although there was a rebound after that but the margin was limited, it is expected that the crude oil trend will maintain its current price volatility and fluctuations, or it will have some support for the spot market. At the beginning of the month, major petrochemical companies introduced new pricing, and prices remained high. However, traders' confidence in the market outlook is obviously insufficient, mainly due to the impact of low demand. In September, the number of factory overhauls and maintenances increased in the next month, and the demand declined significantly. Although the upstream cost determines the market price, there is nowhere to go but there is a market without price. Under the constraints of Lido Lee's many factors, the spot price may be dominated by turbulent prices in the next month.